Northern Ireland weekly market report

and live on Freeview channel 276

17 October 2022

Grains

The dials in this report reflect the analyst’s view of the possible direction in markets. The two-week (solid line) and six-month (dashed line) outlooks are based on the best available information at the time of writing. Please note, these views do not constitute trading advice and direction of markets may change due to new information since the time of writing.

Wheat – Short term, markets remain supported by concerns of Black Sea supply. Volatility is set to continue as new news emerges on the continuation of the export corridor, and of the escalating conflict. Longer term, southern hemisphere production will be a key factor to watch for global supply, and recessionary concerns could pressure markets.

Advertisement

Advertisement

Maize – The war in Ukraine, and tight global supply, are factors keeping markets supported short term. Longer term, with a currently tight global balance, large South American plantings and recessionary impact on demand could loosen this picture slightly.

Barley – Barley markets continue to follow the wider grain complex, supported by supply outlooks remaining tight.

Global markets – Last week global grain markets differed in their movement across the week (Friday to Friday). Price movements continue to be volatile, following news closely on the Black Sea conflict as a key market driver.

Last Monday, nearby Paris and Chicago wheat markets closed at the highest points since June 2022. This support follows the escalation of the missile strikes across Ukraine, following the bombing of the bridge linking Russia to Crimea.

Advertisement

Advertisement

Concerns have also been growing for the renewal of the UN corridor deal with Russia which allows the current flow of exports from Ukraine. This deal is set to expire towards the end of November. On Thursday, Russia’s Geneva UN ambassador said Russia could reject the renewal of this deal. Though talks on Friday between Russia and Turkey were seen by the market as progress on renewing this deal, and as a result we saw some risk taken out of prices. As this situation develops, prices will continue to react.

US wheat markets felt overall pressure last week, despite Ukrainian supply uncertainty, due to a strengthening US dollar and progress seen on Friday for the renewal of the UN export corridor.

Looking to Southern hemisphere production, heavy rains in the Australian east coast have been raising quality concerns for their wheat crop. However, the second largest national wheat crop on record is forecast at 32.2Mt this season (ABARES).

The Buenos Aires Grain Exchange revised their Argentinian wheat crop conditions, to reflect a higher percentage of poor/very poor crops, up 3 percentage points to 49% as at 12 October. This is due to drought and some frost seen across Argentina. Their production forecast was also reduced, down 1Mt to 16.5Mt.

Advertisement

Advertisement

Looking to global maize markets, supported by the Black Sea supply concerns and overall tight supply and demand.

On Wednesday, the USDA lowered US maize yields (due to drought) in the World Supply and Demand Estimates (WASDE) as the market had expected. Maize yields were reduced by 0.03t/acre to 4.34t/acre compared to September’s estimates.

The WASDE still projects 2022/23 Argentinian maize production at 55Mt, but plantings are progressing slowly due to drought according to the Buenos Aires Grain Exchange. As at 12 October, 16.4% was complete. Can we see this production figure revised down?

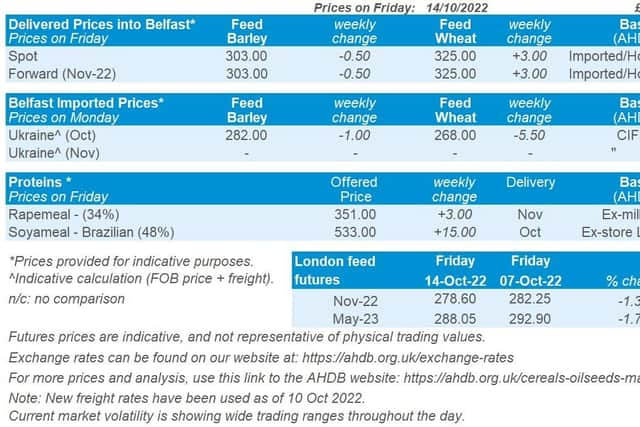

UK focus – UK feed wheat (Nov-22) futures lost £3.65/t across the week, to close at £278.60/t on Friday. This followed Chicago wheat futures down and fell from Monday’s high of £293.20/t, the highest nearby price close since mid-June.

Advertisement

Advertisement

UK delivered prices followed futures contract movement Thursday to Thursday. Feed wheat delivered into East Anglia (February delivery) was quoted at £286.50/t, up £2.00/t.

The pound sterling strengthened slightly by 0.78% against the US dollar Friday to Friday, to close at £1=$1.117. Domestic markets are reacting quickly to the UK’s political news, adding potential further volatility to exchange rates.

On Wednesday, the latest HMRC trade data was released for August figures. From July to August, according to HMRC data, 110.8Kt of wheat has been exported over the two months. This up 81Kt from the same period in the previous year.

Oilseeds – The dials in this report reflect the analyst’s view of the possible direction in markets. The two-week (solid line) and six-month (dashed line) outlooks are based on the best available information at the time of writing. Please note, these views do not constitute trading advice and direction of markets may change due to new information since the time of writing.

Advertisement

Advertisement

Rapeseed – In the short term, rapeseed markets remain reactive to news on the Ukrainian export corridor. Longer term, soyabean markets and recessionary concerns will likely pressure prices.

Soyabeans – Global ending stocks were revised up as expected in Wednesday’s WASDE, easing global S&D despite a smaller US crop. However, planting progression in South America over the next few weeks will be key to longer term direction.

Global markets – Chicago soyabean futures (Nov-22) were up 1.2% over last week (Friday to Friday). Whereas Chicago soyabean oil futures (Dec-22) were down 2.0% over the same period, tracking the price movement of Brent crude oil prices.

US soyabean crushing in the month of September is expected to have reached an all-time high for this time of year, as processors have increased production with newly harvested US beans now on the market. Ahead of the monthly National Oilseed Processors Association (NOPA) report due out later today, analysts are expecting 4.4Mt to have been crushed last month (Refinitiv). If realised, this would be down 2.4% from August, but up 5.1% on the year. Analysts are also predicting that soya oil supplies held by NOPA members, as at 30 September, will be down 2.7% from the previous month and down 9.6% year-on-year. While we could see some support as a result, reduced yearly export demand (down 5.2% on the year) will likely outweigh increased domestic crushing demand.

Advertisement

Advertisement

In the latest WASDE released on Wednesday, US soyabean yields were unexpectedly pulled back to 1.33t/acre, resulting in production being cut to 117.38Mt. This is down 1.5% from September’s estimate. While reduced from previous estimates, this figure is still higher than both the 5-year and 10-year US production average. The cut in US production was also outweighed by a drop in export demand, and world ending stocks were revised up 1.6% from the previous month. Read more information in Thursday’s Grain market daily.

Brazilian soyabean plantings are underway and at the end of the week commencing 03 October, plantings were 10% complete, ahead of the 8% average for this point in the season (AgRural).