The NI market report

and live on Freeview channel 276

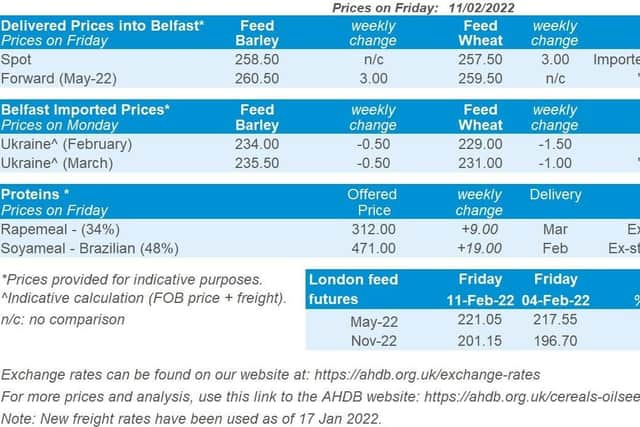

Grains

Wheat - A relatively cautious USDA report leaves the short-term picture drifting, but the sentiment could turn bullish if Russian-Ukrainian tensions escalate. Longer-term, there is expectation for some recovery in output, although Canadian areas and soil moistures will need to be monitored come Spring.

Maize - Global reliance on South American crops still stands, where the Safrinha crop is only just being planted. However, there is also uncertainty around the US 2022 area, leaving the market awaiting some new news.

Advertisement

Advertisement

Barley - Barley tends to track wheat markets and again, Canadian planting intentions will be one to watch. If North Africa remains dry, it could increase barley import demand, in turn offering support to prices.

Global markets

Last week’s USDA report gave limited direction to markets, but prices still ended the week higher. Many within the trade suggest the USDA’s South American crop cuts were too cautious. There is an expectation for estimates to be reduced further in the coming months. Conab, Brazil’s official forecaster, cut 0.6Mt from its maize forecast pegging it 1.7Mt lower than the USDA estimate, at 112.3Mt.

The Chicago May-22 maize futures contract gained $11.32/t across the week (Friday-to-Friday) despite the USDA’s bearish estimates. Closing the week at $256.10/t, it reached an all-time contract high. New crop (Dec-22) also closed the week on a contract high of $234.15/t, up $8.26/t from the previous Friday.

Wheat markets also found support last week. Friday saw a jump in global wheat markets on the back of increased concerns about a possible Russian invasion of Ukraine potentially disrupting exports. Both countries are major exporters of wheat. They are expected to make up 29% of global wheat exports combined in 2021/22 (USDA). This means any disruption to exports would inevitably cause global availability issues. Russia and global media accuse the US of causing panic but the situation is aiding market sentiment and will be a watch point.

UK focus

Advertisement

Advertisement

UK feed wheat futures followed trends in global markets. Friday saw a jump up in both May-22 and Nov-22 values, closing the week at £221.05/t and £201.15/t respectively.

Despite a week-on-week price rise for delivered bread wheat into the North West, the premium over May-22 futures squeezed further (May delivery). The premium was £66.50/t over feed wheat futures on Thursday (10 Feb) versus £68.00/t the week before.

The survey quoted a new crop (Nov-22) bread wheat price for the first time this year in Friday’s report. November delivery of bread wheat into Northampton averaged £238.00/t, or c.£38.00/t over futures. The premium at the same point last year (versus Nov-21 futures) was just £27.00/t. This indicates some nervousness for bread wheat availability next marketing year.

Oilseeds

Rapeseed - Old crop supply remains tight until the Northern Hemisphere harvests. Canadian planting intentions will drive sentiment but currently production is anticipated to rebound for the 2022/23 marketing year.

Advertisement

Advertisement

Soyabeans - Downward revisions to South American crops, combined with tightening global supply and demand supports soyabeans. There could be longer-term support if the US new crop is delayed or experiences adverse weather.

Global markets - The Chicago soyabeans May-22 contract gained 1.8% from Friday-to-Friday, to close at $582.79/t.

Driving this gain is the on-going dry weather curbing soyabean production from South America. Last week there were cuts from the USDA to Argentinian (-1.5Mt) and Brazilian (-5.0Mt) soyabean production estimates.

Further to that, Conab slashed Brazilian soyabean production by 15.0Mt in its monthly update. It now estimates the crop at 125.5Mt, citing dry weather in the southern states as the reason for the cut.

Advertisement

Advertisement

Commodity funds were net-buyers of Chicago soyabeans future contracts over the last week. Further support for soyabean prices has been the run of US export sales. Between 04 and 10 Feb over 1.8Mt of old and new crop soyabean sales have been reported to China and unknown destinations.

The focus over this next week will continue to be South American conditions. Argentina is expecting some rain but temperatures remain hotter-than-usual in parts. Brazil is expecting widespread rains over the next week, which could delay the harvest.

Another factor driving edible oil markets is Brent crude oil. The nearby contract rose 3.3% on Friday closing the week at $94.44/barrel. Support in oil comes from fears Russia could invade Ukraine, disrupting energy exports.

Rapeseed focus

Paris rapeseed futures (Aug-22) closed Friday at €619.00/t, gaining €16.00/t across the week. UK delivered rapeseed (into Erith, hvst-22) was quoted at £515.00/t, gaining £1.00/t across the week.

Advertisement

Advertisement

UK prices did not encapsulate the same gains as Paris futures because our delivered survey was conducted late morning on Friday and Paris rapeseed futures were volatile throughout the day. The Aug-22 futures contract traded in a €9.25/t range.

Further to that, Sterling strengthened (+1.11%) against the Euro across the week, closing Friday at £1 = €1.1941.