NI Weekly Market Report

and live on Freeview channel 276

07 November 2022

Grains

Wheat

Markets remain volatile as they await news on the future of the Ukrainian export corridor. Prices stay supported but market optimism keeps gains limited. Adverse weather in the Southern Hemisphere is causing concerns over production.

Maize

The global maize outlook remains tight, and markets are reactive to the situation in Ukraine. Forecasts of improved weather over South America could see further planting progress over the next week.

Barley

Advertisement

Advertisement

Barley markets continue to follow the wider grain complex, supported by tight outlooks.

Global markets

While remaining volatile, global grain markets were supported across last week. Chicago wheat (May-23) and Paris milling wheat (May-23) were up 2.0% and 0.4% respectively Friday to Friday. Chicago maize (May-23) climbed 0.1% over the same period.

Prices saw a steep rise at the beginning of the week due to Russia announcing they would no longer participate in the Ukrainian grain corridor agreement. However, prices fell mid-week as Moscow said they would re-join the export deal. Losses were capped though, as support came from Southern Hemisphere production concerns (more on Argentina and Australia below).

On Wednesday, Putin announced that Russia would not hinder grain supplies from Ukraine to Turkey “at any point in the future”, providing that guarantees from Ukraine that export routes would not be used for military means, were not violated. Turkey’s foreign minister has also said that Russia is eager to export more of its own agricultural products including fertiliser and grains, but that ships of many countries are hesitant about transporting Russian cargo. With the export deal initially agreed for 120 days ending this month, markets will remain reactive to news of the potential extension of the deal over the next couple of weeks.

Advertisement

Advertisement

The Buenos Aires Grain Exchange cut Argentina’s 2022/23 wheat harvest to 14Mt on Thursday, down from its previous estimate of 15.2Mt. Prolonged drought, combined with extended frosts over the beginning of last week in the country’s main wheat growing regions, are the reasons for these further production trims. The Exchange also said on Thursday that 2022/23 maize plantings had advanced by 1.1% across the week, with 22.9% of the estimated 7.3Mha planted area complete as at 02 November. Forecasted rains over the next week could mean conditions for maize plantings improve, but this is arguably too late for the wheat crop. The USDA’s most recent World Agricultural Supply and Demand Estimates (WASDE) will be released on Wednesday (09 Nov), and changes to the Argentinian wheat production figure will be something to look out for.

While still on track for a third bumper harvest, excessive rains and subsequent flooding in Australia is impacting quality expectations. According to Refinitiv, around half of the wheat crop grown on the eastern grain belt is expected to be reduced to animal feed. However, it’s thought that the full extent of the damage to crops will not be known until the waters recede. With more rain forecast over the next 7 days in certain eastern regions, the quality of the Australian wheat crop will be something to monitor going forward.

UK focus

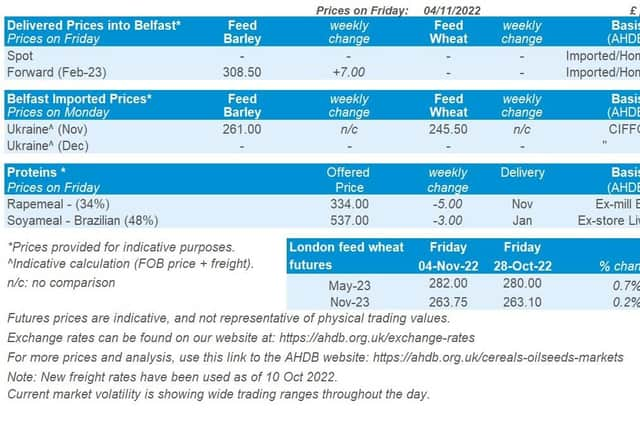

UK feed wheat futures tracked global markets up last week. The May-23 contract gained 0.7% over the week (Friday to Friday). New crop prices (Nov-23) gained slightly less, up 0.2% over the same period.

Domestic delivered prices followed futures price direction up. Feed wheat into East Anglia for November delivery was quoted at £272.50/t on Thursday, up £6.00/t on the week. Bread wheat prices for November delivery into the North West were quoted at £344.50/t, up £4.50/t on the week.

Oilseeds

Rapeseed

Advertisement

Advertisement

In the short-term, price direction will depend on the continuation of the export corridor, though continued volatility is expected. Longer term, large soyabean supplies could weigh on the wider oilseed complex and pressure prices.

Soyabeans

Short term, markets are expected to move on news on the Black Sea corridor, Brazilian politics and rains in Argentina. Long term sentiment there is large South American crops expected. But on-going dry weather in Argentina, and Chinese lockdowns, remain watchpoints.

Global markets

Last week saw support for Chicago soyabeans futures (May-23), as the contract gained 4.2% across the week to close Friday at $542.28/t.

Support in oilseeds came from strong energy prices, due to uncertainty around future US interest rate hikes by the Federal Reserve, combined with the EU reducing reliance on Russian oil. This support resulted in nearby brent crude oil futures gaining 2.9% across the week.

Advertisement

Advertisement

Further to that, supporting soyabean markets were blockades in Brazil as protests escalated as Bolsonaro lost the presidential election to Lula, this put concerns over food exports out of the country.

Also, there was support from Chinese demand optimism, as there were rumours last week that China would ease their strict Covid-19 restrictions. However, this optimism hasn’t come into fruition today, as China denied all indications that they would be easing their zero-covid policy leading to marginal pressure for Chicago soyabeans today.

Chinese demand is a key parameter to oilseed market direction. Last week, the latest USDA Attaché report on oilseeds kept China’s soyabean import forecast at 96.5Mt for 2022/23. Lower than USDA official estimates and lower on 2020/21 imports, but higher than last season (2021/22) due to higher demand in animal feed and vegetable oil for the food sector.

For oilseed supply, plantings in Argentina are not off to the best start due to drought from the third successive La Niña weather event. Latest reports from Rosario Grains Exchange suggest that due to the lack of moisture, farmers are looking to reduce their fertiliser use.

Rapeseed focus

Advertisement

Advertisement

Rapeseed prices were supported last week with the oilseed complex, as Paris rapeseed futures (May-23) closed Friday at €660.00/t, up €23.00/t across the week.

Delivered rapeseed (into Erith, May-23) was quoted on Friday at £587.00/t, gaining £30.50/t over the week. Greater gains were seen on the domestic market, as the sterling weakened (-2%) against the euro across the week, to close Friday at £1 = €1.1416.