NI weekly market report - 14 August 2023

and live on Freeview channel 276

August 14, 2023

Grains

Wheat

Black Sea news keeps markets volatile and supported, as the market assesses how accessible Ukrainian supplies are. Global supply remains finely balanced to demand, but if large maize supplies are realised and Black Sea wheat continues to be competitive, we could see prices pressured.

Maize

US weather watching continues short term, for the US crop that is starting to dent. Though longer term, large South American crops and the second largest recorded US crop is due, boosting supplies.

Barley

Advertisement

Advertisement

With tight global barley supplies, feed barley prices find support from wider grains. However, like wheat, a large global maize supply could weigh on prices longer-term.

Global markets

Last week saw mixed movements across global grain contracts, with overall pressure seen across Chicago wheat and maize contracts, though a price rise on Paris milling wheat futures. Despite some gains early last week on Black Sea supply concerns from the ongoing war, price losses later in the week followed due to news of competitive Russian wheat and the latest USDA World Agricultural Supply and Demand Estimates (WASDE) being released.

On Friday the latest USDA WASDE was released, trimming global ending stocks for 2023/24 for both wheat and maize, though this was expected by the market. Global wheat production was reduced 3.3 Mt from last month’s estimates, mostly on smaller crops in Canada, EU, and China despite a bigger Ukrainian crop forecast.

Global consumption was also trimmed back, though global wheat ending stocks still fell on the month, now down 2.7 Mt on the year and at the lowest level since 2015/16 at 265.6 Mt. US wheat export forecasts were trimmed back for this season slightly by 680 Kt, this weighed on US wheat markets.

Advertisement

Advertisement

Global maize ending stocks for 2023/24 were trimmed to 311.0 Mt, with cuts made to both global production and consumption in comparison to last month’s estimates. Though global maize ending stocks remain over 13 Mt higher year-on-year. The US maize crop was cut back 5.3 Mt to 383.8 Mt on account of using the first survey-based yield forecast. Though the crop remains the second largest on record.

Competitive Russian wheat continues to weigh on global wheat markets. Last week, Egypt’s state buyer GASC purchased 235 Kt of Russian wheat, despite an increase in freight costs from the region over the week.

Markets remain reactive to news on Black Sea shipping, with the active war ongoing in Ukraine and larger crops forecast.

Ukraine is looking to form safe shipping routes in the Black Sea and has started to register ships willing to use the corridor, as reported by a local news agency on Saturday

Advertisement

Advertisement

Though on Sunday, a Russian warship fired warning shots at a cargo ship in the southwestern Black Sea heading north.

EU quantity and quality concerns remain in focus, after heavy rain across northern Europe. Last week consultancy Stratégie Grains trimmed wheat and maize forecasts for harvest 2023.

UK focus

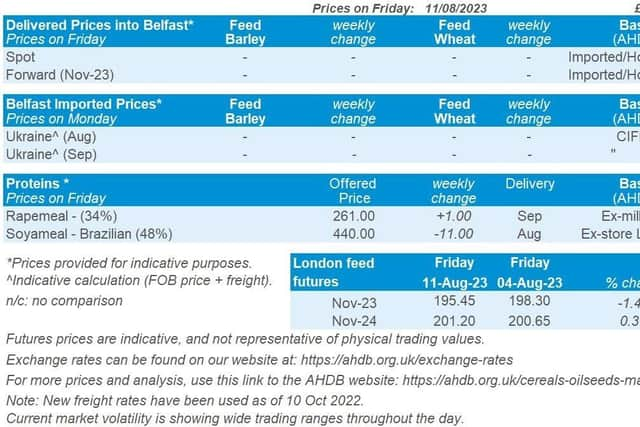

UK feed wheat futures (Nov-23) ended down £2.85/t last week, to close on Friday at £195.45/t.

Following US contracts, gains early in the week were retraced at the end of the week. The Nov-24 contract closed at £201.20/t on Friday.

Advertisement

Advertisement

Domestic delivered prices followed futures movement (Thurs to Thurs) at a slight gain on the week.

Feed wheat delivered into East Anglia (September delivery) was quoted on Thursday at £194/t, up £1.50/t on the week.

North West bread wheat (September delivery) also gained the same amount on the week, to be quoted on Thursday at £272/t.

GB harvest is progressing slowly, with mild and wet weather continuing for many. Winter barley harvest was 94% complete to week ending 08 August, about on par with the five-year average.

Advertisement

Advertisement

Harvest of winter wheat, spring barley and oats were all 5% complete to the same date, well behind the five-year averages. Overall crop quality is variable between regions.

This past week we have seen some more favourable weather, and another report is provisionally forecast for this Friday to assess progress (18 August).

The latest GB fertiliser prices were released last week, quoting UK AN at £353/t for July, up £9/t from the previous month.

Oilseeds

Rapeseed

Despite marginal cuts to Canada’s canola crop, the global rapeseed market is well supplied.

Advertisement

Advertisement

Longer-term pressure on soyabeans will filter into the rapeseed market, but conflict in the Black Sea could offer short-term support.

Soyabeans

Tighter US ending stocks could offer some support to markets in the short-term, but confidence is growing for the US soyabean production.

Longer-term large South American crops are expected going into 2024 which will weigh on oilseed markets.

Global markets

Chicago soyabean futures (Nov-23) were pressured 2.0% across the week, closing Friday at $480.38/t, the third successive week of declines for the contract.

Advertisement

Advertisement

Pressuring the market at the start of the week was improving US soyabean crop conditions, combined with the forecast of better weather in the US.

Last Monday’s USDA crop progress report (to week ending 06 Aug) estimated 54% of US soyabeans good-to-excellent, up from 52% the week before.

The contract then saw some support throughout the week due to demand for US origin soyabeans and traders squaring positions ahead of the USDA World Agricultural Supply and Demand Estimate (WASDE), which was released on Friday.

The USDA reported US export sales of (old and new crop) soyabeans totalled 1.5 Mt (to week ending 03 Aug). A large proportion of new crop soyabean sales were to China, who purchased 753 Kt for the 2023/24 marketing year, with 314 Kt reported to unknown destinations.

Advertisement

Advertisement

Traders adjusted positions ahead of the August WASDE report. In the report, US soyabean production was trimmed by 2.6 Mt from last month, to 114.5 Mt. The downward revision was due to dry conditions early in the growing season, impacting yield potential.

This revised estimate was below the average trade estimate at 115.6 Mt. This revision means that US ending stocks for 2023/24 are now estimated at an 8-year low of 6.7 Mt. Initially the market was supported on Friday from this news, but later settled as downward revisions were expected to this US soyabean crop.