Northern Ireland weekly market report

and live on Freeview channel 276

Grains

Wheat - News of decent production nearing confirmation in the Southern Hemisphere and lagging US export sales could pressure markets. However, the global supply and demand balance remains tight. The market now awaits the USDA report for strong direction.

Maize - Expectation of smaller maize crops from South America offers support to the market which, if realised, will offer support until northern hemisphere harvests start again in the new marketing year.

Advertisement

Advertisement

Barley - Barley markets generally track wheat market movements with a relatively tight discount.

Global markets - The two key grain markets moved in opposite directions last week. From Friday-to-Friday, Chicago maize futures (May-22) gained $5.02/t to close at $239.27/t. However, across the same period, Chicago wheat futures (May-22) lost $5.05/t to close the week at $279.41/t. Paris (May-22) milling wheat lost €4.75/t across the week closing at €272.00/t. London feed wheat closed the week at £218.50/t, down £6.00/t from the previous Friday’s close.

All markets await the USDA world agricultural supply and demand estimates (WASDE) out this Wednesday evening, but speculations are already made.

The global wheat supply for 2021/22 is almost confirmed with Argentine and Australian harvests nearing completion. Both countries are anticipated to have bumper volumes this season. This, coupled with slow US export sales have weighed on wheat markets recently.

Advertisement

Advertisement

There are concerns, particularly for maize (and soyabean) crops in South America, although the first crop is not as vast as the second (Safrinha) maize crop. Early-sown maize crops are going through key growth stages as extreme weather hits. The Argentine weekly crop conditions report (06 Jan) shows maize crop conditions have dropped further, with 21% of the crop now classed as poor/very poor versus 8% the week before.

Brazil has also suffered weather concerns although it received more rain over the past month than Argentina, particularly in the northern regions. In Brazil, the second crop, due to be planted after the soyabean harvest, is the most significant in volume. But, if current dryness continues this crop will have a disadvantaged start.

Average industry expectation, according to a Refinitiv poll, is for the Brazilian and Argentine crops to be reduced by a combined 2.7Mt in the upcoming USDA report. Even still, this would be record crops from both countries. Although there is some level of reduction priced into markets, if the USDA reduce the production estimate more than expected, we could see a further spike in prices. Conversely, a smaller reduction could be negative for prices.

UK focus - UK feed wheat slipped last week following losses in Paris and Chicago wheat markets. Despite a slight lift on Friday, the May-22 (London feed wheat) contract closed the week down £6.00/t at £218.50/t. The new-crop contract (Nov-22) also closed lower on the week at £191.55/t, down £4.95/t from the previous Fridays close.

Advertisement

Advertisement

Delivered bread wheat into the North West in January was quoted at an average price of £282.50/t on Thursday last week. This is a £4.00/t drop from the previous survey (16 Dec 2021) but up £44.50/t from the same time last year (07 Jan 2021).

Delivered feed wheat into East Anglia (Jan delivery) is also down £4.00/t from the previous survey at £214.00/t but only £8.00/t higher than the first week in January 2021.

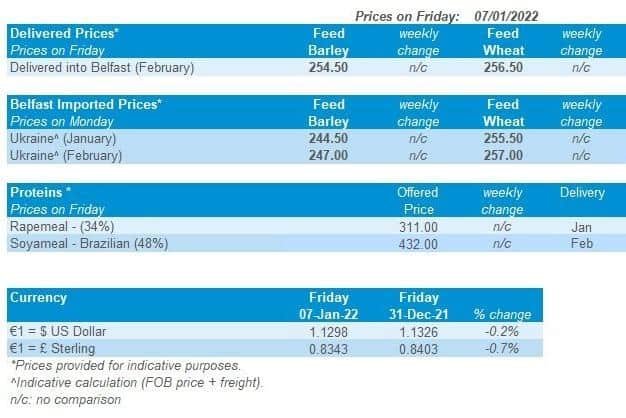

In the Avonrange area, the average price of delivered feed barley for February delivery is £214.50/t. This is just £3.00/t under delivered feed wheat into the same area.

Oilseeds

Rapeseed - Global tightness in rapeseed markets keeps old crop values inflated. Longer-term supply is anticipated to recover, but general market direction will largely be dictated by soyabeans.

Advertisement

Advertisement

Soyabeans - There is notable dryness in Argentina and southern parts of Brazil, which is supporting the market. Sentiment longer-term is unchanged as any production losses in South America are not yet confirmed.

Global markets - Chicago soyabean futures (May-22) gained 5.2% last week. South American weather is dominating market news, and commodity funds were net buyers of soyabeans last week.

Dry weather, notably in Argentina and southern parts of Brazil, is cited to be impacting on soyabean crops. Analysis by Bank of America Securities notes that soyabean production in southern regions of Brazil could drop by 8%. Further to that, rains in the centre west region of Mato Grosso are delaying the initial progression of harvest.

Several agricultural consultancies have already cut Brazil soyabean production. AgRural pegs the crop at 133.4Mt, down from 144.7Mt. StoneX estimates the production at 134Mt, down around 11.0Mt from its December 2021 estimate.

Advertisement

Advertisement

The market now awaits the latest USDA supply and demand estimate out this Wednesday (12 Jan). Industry expectations are for minor downward revisions of South American crops, but nothing too drastic (Refinitiv poll).

Furthermore, demand for soyabeans remained strong last week with 354Kt of US sales booked for both old and new crop shipment. The destinations were Mexico and ‘unknown’.

Malaysian palm oil futures (Mar-22) gained 6.3% across the week following on-going concerns that adverse weather will impact output. Furthermore, the latest data released today, estimates that Malaysia’s December ending stocks of palm oil dropped to 1.58Mt. This is down 12.9% compared to November.

Rapeseed focus - Old crop Paris rapeseed futures (May-22) closed Friday at €758.50/t, gaining €46.75/t across the week. New crop values (Aug-22) closed at €592.00/t, gaining €38.00/t across the week.

Advertisement

Advertisement

Support in soyabean markets is filtering into rapeseed prices. Delivered rapeseed (into Erith, Harvest-22) was quoted at £480.00/t last Friday, with no comparison week-on-week.

Sterling continued to strengthen across the week (+0.53%) against the Euro. Trading closed Friday at £1 = €1.1962.