Northern Ireland weekly market report

and live on Freeview channel 276

Grains

Wheat - In the short-term, prices continue to respond to maize market movement and Ukrainian export news. Tight global grain supplies continue to support markets in the longer-term.

Maize - Lower global supplies are supporting markets in the short-term and long-term. Demand remains a watchpoint now for price direction.

Advertisement

Advertisement

Barley - Barley markets continue following the wider grains complex, with supply outlooks remaining tight.

Global markets - Global grains saw overall pressure last week. Despite gaining support through the week, global contracts lost ground on Friday and yesterday.

Some support last week came from the USDA trimming global maize production for 2022/23 by 7Mt to 1,172.6Mt in their recent World Agricultural Supply and Demand Estimates (WASDE) report. This was due to reductions in US and EU production.

The European Commission have reduced their maize yield forecasts again, due to recent drought conditions, with recent rains too late to make a significant difference. As such, in the September report, EU maize yield estimates were reduced 4% on August’s estimate to 6.39t/ha, which is now 19% under the five-year average. Downward revisions to EU maize have also been seen in the recent Stratégie grains report, with production now at 52.9Mt. This is down 2.5Mt from August’s estimate.

Advertisement

Advertisement

However, overall global grain markets felt pressure last week on demand concerns. Increased interest rates to tackle inflation created some broad-based selling, as concerns grow for slow global economic growth.

Yesterday, global wheat markets felt further pressure too as IKAR revised Russian wheat production forecasts up 2Mt, to 99Mt.

According to FranceAgriMer and Arvalis, French milling wheat average protein content is down 0.5 percentage points on last year, at just 11.4%. This is a similar story to our domestic quality, as seen in the Cereal Quality Survey provisional results.

UK focus

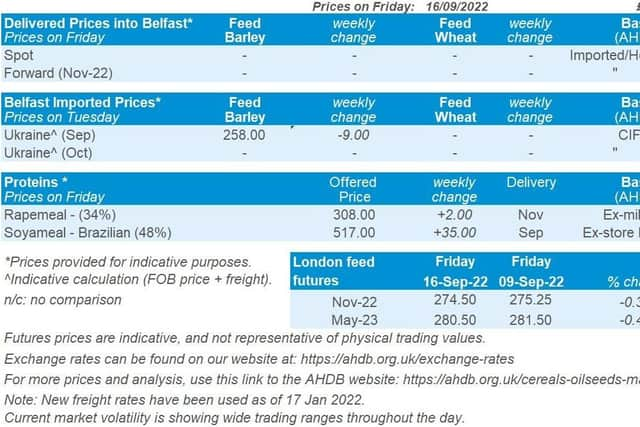

Due to the bank holiday for Queen Elizabeth II funeral, UK feed wheat futures did not trade yesterday. The Nov-22 contract was down £0.75/t across last week, closing at £274.50/t on Friday. The Nov-23 contract closed at £263.20/t, losing £1.70/t Friday-Friday.

Advertisement

Advertisement

East Anglia delivered feed wheat prices for September delivery were quoted at £269.50/t on Thursday, up £5.00/t on the week. This price increase mirrors UK feed wheat futures movements (Thursday-Thursday).

Bread wheat delivered into the North West for October was quoted at £334.50/t, up £4.50/t Thursday to Thursday.

According to HMRC’s most recent trade data (12 Sep), in July the UK exported 51.5Kt of wheat and 100.3Kt barley to the EU. Compared to the same point last year, this is up 35.2Kt and 86.6Kt respectively.

Our sixth and final harvest report came out on Friday. Harvest is all but complete, with some crops still to harvest in Scotland. Following the extended period of dry weather, recent rainfall across most of GB has had little impact on progress or quality. Although this has been variable. To note, there are increasing reports of Ergot in East Midlands in winter and spring wheat samples, and small amounts in winter and spring barley samples. However, overall, there have been limited amounts found in central stores.

Oilseeds

Advertisement

Advertisement

Rapeseed - Short-term harvest pressure from Canada’s canola crop and US soyabean will be expected. Longer-term rapeseed market for 2022/23 will be much more influenced by the greater oilseed complex with a larger Canadian canola crop.

Soyabeans - Despite lower US production, harvest pressure is expected over the coming weeks. Recessional fears still play into demand fears. Furthermore, record South American crops expected start of 2023.

Global markets - Chicago soyabean futures (Nov-22) were supported (+2.6%) across last week, Friday to Friday. With the US market open yesterday, Chicago soyabean futures (Nov-22) started the week supported (+0.9%) further to Friday’s close from renewed export sales of 136Kt of soyabeans reported to China through its daily reporting system. Something to watch considering ongoing demand worries from global recessionary fears.

The soyabean market weekly gain last week, was on the back of the latest USDA World Agricultural Supply and Demand Estimate (WASDE) report. In the report, US soyabean production was reduced 4.1Mt to 119.2Mt on lower area and yield. This led to a fall in forecasted global ending stocks, read more on this report here.

Advertisement

Advertisement

Following Monday’s (12 Sep) support, the market dropped for the next 4 trading sessions. Driving this marginal pressure was the favourable weather conditions in the US, which has helped to mature the soyabean crop and for harvest to start. The latest USDA crop progress report (up until 18 Sep) estimates US soyabean harvest at 3%, below last year and the five-year-average of 5%. The slower harvest is reflecting the delayed sowing in May/June time.

In other news, Argentine growers have increased sales of their 2021/22 crop which they have been holding on to. This is after the government implemented a favourable exchange rate for them to market their soyabeans, increasing the amount of soyabeans on the market. Plantings of soyabeans is starting in the Mato Grosso region of Brazil on irrigated soils, with Ag Rural estimate 42.7Mha to produce a record crop of 148.5Mt for the 2022/23 season.

Rapeseed focus

Quite the opposite happened in rapeseed markets with Paris rapeseed futures (Nov-22) closing Friday at €577.25/t, down €20.50/t across the week. Domestic prices shadowed this loss with delivered rapeseed (into Erith, Nov-22) being quoted at £503.00/t, down £22.00/t week-on-week.

With the market open yesterday, prices were further pressured with Paris rapeseed futures (Nov-22) closing at €571.50/t down €5.75/t on Friday’s close.

Advertisement

Advertisement

Limited rain across the Canadian Prairies over the last 7-days has allowed harvest to progress which pressured the market.

Latest statistics (released 14 Sep) from Statistics Canada estimate the 2022 canola (rapeseed) crop at 19.1Mt. This is up 38.8% from 2021. This prediction is based on satellite and agroclimatic data with consistent rains and warm temperatures this year, allowing the annual increases in crop production.