Northern Ireland weekly market report – 4 September 2023

and live on Freeview channel 276

4 September 2023

Grains

Wheat

Markets will remain reactive to any news on Black Sea supplies. Global supply and demand looks to be tightening, though plentiful maize supply will likely pressure feed wheat markets longer term. The outlook for milling prices will depend on quality results from Northern Hemisphere harvests.

Maize

US weather remains a watchpoint in the short term. Longer term, large US and Brazilian crops will likely weigh on the market.

Barley

Advertisement

Advertisement

Due to plentiful maize supply expectations, the feed grain market seems well supplied. Barley will continue to follow the wider grains market.

Global markets

Global wheat and maize markets were overall pressured last week. Chicago wheat futures (Dec-23) were down 4.2% Friday to Friday. Chicago maize futures (Dec-23) were down 1.3% over the same period.

Much of the pressure at the beginning of the week was a result of better-than-expected US crop condition scores published last Monday. Despite ongoing hot and dry weather, 56% of the US maize crop was rated good-to-excellent, a smaller decline than predicted by analysts (Refinitiv). As most crops are still to mature, adverse weather could still impact yield potential over the next couple of weeks. Over the next seven days, temperatures are expected to remain unseasonably high. Though there is forecast to be some welcome rain in the US Midwest, this will remain something to watch.

Talks between Turkish President Erdogan and Russian President Vladimir Putin are expected to take place today in Sochi. It’s reported that the Turkish President will try to convince Putin to return to a Ukrainian grain export deal. The previous deal expired in July. Grain markets will remain reactive to any news on this over the next few days.

Advertisement

Advertisement

Competitive Russian grain supplies continue to weigh on the global market. Egypt’s General Authority for Supply Commodities (GASC) bought around 480 Kt of Russian wheat on Friday in a tender. The wheat was bought for c.$270/t, with traders reporting this could be below the unofficial floor set by Russia’s government (Refinitiv).

The Australian Bureau of Agricultural and Resource Economics and Sciences (ABARES) is due to release its latest crop forecasts tomorrow. Analysts and traders are expecting Australia to lower its wheat production forecast for 2023/24 by around 1 Mt from June’s estimate of 26.2 Mt (Refinitiv). The anticipated cut to production is a result of the El Niño weather event reducing yields. More analysis will be available on this in tomorrow’s Grain market daily.

UK focus

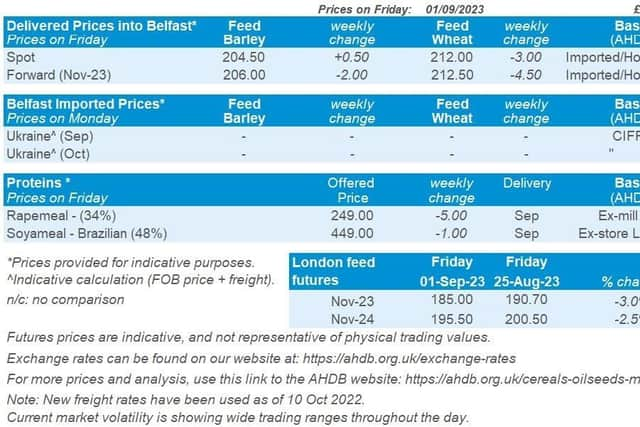

UK feed wheat futures followed global price movement down last week. The Nov-23 contract fell £5.70/t last week to close on Friday at £185.00/t. The Nov-24 contract closed at £195.50/t on Friday, down £5.00/t over the same period.

Delivered feed wheat prices followed futures price movement Thursday to Thursday last week. Feed wheat delivered into East Anglia for November delivery was quoted at £187.00/t, down £3.00/t. Reports suggest UK milling wheat quality is very variable, and this is reflected in delivered bread wheat prices. Bread wheat delivered into the North West for November delivery was quoted at £268.00/t on Thursday, down £5.00/t on the week. This price was at a £82.00/t premium to Nov-23 UK feed wheat futures, historically high for this time of year.

Advertisement

Advertisement

Drier weather over the past two weeks allowed the GB harvest to make good progress, says the latest AHDB harvest progress report. However, the report also shows variable quality, including some lower Hagberg Falling Numbers (HFN) for winter wheat and germination levels for spring barley. Read the full report here.

On Thursday, Defra released its arable crop areas for England as at 1 June 2023. The stand-out for this data release is the lower-than-expected wheat area for the 2023 harvest, estimated to be 1,580 Kha, down 5% on the year. The total barley area in England for 2023 is estimated at 799 Kha, up 2% on the year. Over the coming weeks, there will be further analysis and insight from these figures on what domestic availability could be for 2023/24.

Oilseeds

Rapeseed

Despite cuts to Canadian and EU crops, the global rapeseed market is well supplied for 2023/24. Longer-term, price direction will largely be dictated by the soyabean market direction.

Soyabeans

Short-term, US weather is the driver as the crop is in critical development stages. The longer-term price direction is bearish, with large South American crops expected into 2024.

Global markets

Advertisement

Advertisement

It was a week of pressure for Chicago soyabean futures. The Nov-23 contract ended down 1.3% across the week, closing Friday at $503.06/t. The main driver was that US soyabean crop conditions were not as bad as anticipated, plus traders were squaring positions before the end of the month. There was slight support on Friday as the focus was on tighter US ending stocks.

Although there was a weekly decline for soyabeans, the Nov-23 contract still gained 2.8% across the month of August. The rise is from the hot and dry weather across the US Midwest, which has posed questions over crop damage. There has also been strong export demand for US-origin soyabeans.

Last Monday (week ending Aug 27), the USDA rated 59% of the US soyabean crop as in good-to-excellent condition, down 1% from the week before. Markets subsided as there were expectations that this rating would have dropped by 3% (Refinitiv).

US export sales (to week ending Aug 24) were pegged at 1.1Mt, in line with trade expectations. Demand remains buoyant for US soyabeans, which could tighten US soyabean ending stocks for 2023/24 even further. This is keeping the US market supported.

Advertisement

Advertisement

In other news, StoneX upped its estimate of the 2023/24 Brazilian soyabean crop to 163.6 Mt, up from 163.4 Mt. This is further adding to this bearish outlook longer term.

There was support across the week for Malaysian palm oil futures. There has been hot and dry weather in the region recently from the El Niño weather event intensifying, which could hinder supply from the region. There is also high demand from the festive season in India.

Rapeseed focus

Paris rapeseed futures (Nov-23) closed Friday at €473.50/t, gaining €0.25/t across the week. Futures came under pressure at the start of the week but recovered towards the end of the week.

Delivered rapeseed (into Erith, Nov-23) was quoted Friday at £389.00/t, down £1.50/t across the week.