The NI weekly market report

and live on Freeview channel 276

Grains

Wheat

Northern hemisphere harvests are accelerating, putting pressure on prices. Longer term, the fundamentals remain supportive with a tight supply outlook.

Maize

While US production looks more optimistic with a higher acreage than anticipated, global supply remains tight. The next few weeks will be critical for crop progression and yield expectations.

Barley

Advertisement

Advertisement

Global and domestic balance remains tight and continues to follow the sentiment of international grain markets.

Global markets

Global wheat markets fell sharply at the end of last week. US wheat fell to levels seen before the conflict broke out in the Black Sea region at the end of February. Chicago wheat futures (Dec-22) ended the week at $316.88/t, down $32.98/t Friday-Friday.

Last week saw some optimism for Ukrainian grain exporters, as we saw grain shipments begin to flow from the region. This, combined with an accelerating wheat harvest across the northern hemisphere, put pressure on global prices last week.

US prices also felt pressure from a firmer US dollar and some risk-off trading on Friday before the long Independence Day weekend. Chicago maize futures (Dec-22) were down $26.18/t over the course of the week, closing at $239.17/t on Friday. The global maize market also reacted to the revised US acreage estimates released on Thursday. Maize area was slightly higher than anticipated, also contributing to a less supported maize market. US weather will continue to be a watchpoint this week as the crop heads into the pollination phase, making it sensitive to moisture and temperature stresses.

Advertisement

Advertisement

Global maize markets also lost some support last week after Stonex increased Brazil’s 2021/22 total crop estimate to 119.3Mt, up 2.5Mt from their previous forecast. They also reported that exports for the month of June were at 1.1Mt, 960Kt higher than the previous year’s figure.

UK focus

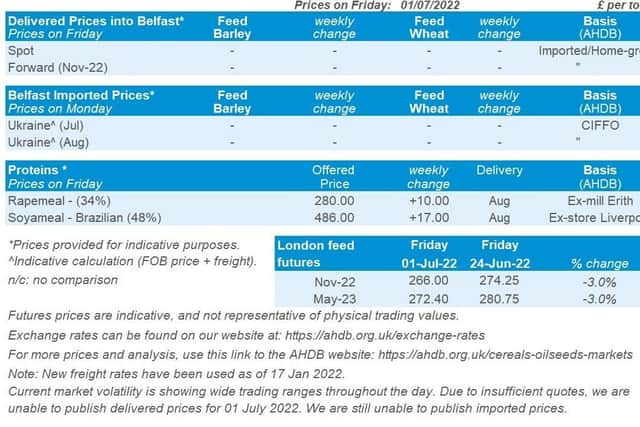

In the domestic market, UK feed wheat futures continued to edge lower last week following the global market as Northern Hemisphere new-crop harvests progress.

The Nov-22 contract closing at £266/t on Friday, down by £8.25/t on the Friday before. The May-23 contract closed at £272.40/t, down by £8.35/t during the same timeframe.

For delivered prices, the East Anglia (Hvst-22) price was quoted at £269.50/t, with no comparison on the week. The last price quoted for this location was published on 16 Jun at £306.50/t. Delivered harvest prices have shadowed the drop in the global market since this time.

Advertisement

Advertisement

Meanwhile bread wheat prices in the North West (Nov-22) were quoted at £342.50/t, with no comparison on the week. This is at a £66.95/t premium to the UK feed wheat futures based on Thursday’s close (£275.55/t). This price is down on the last published quote (16 Jun) for this location and month which was £377/t, with premiums over feed wheat futures slightly lower at £65.70/t.

Oilseeds

Rapeseed

Rapeseed prices have been pressured with the wider oilseed complex in the short-term. Long term prices will be more influenced by other oilseeds in the 2022/23 marketing year, along with an anticipated increase in Canada’s canola crop.

Soyabeans

Soyabean prices in the short-term will be reactive to U.S. weather, with no great concerns currently. Long-term focus will be on South American planting intentions and whether high input prices will reduce acreage.

Global markets

Chicago soyabean futures (Nov-22) ended down $10.66/t across the week, closing at $512.61/t. This contract is now back down to pre-war levels.

Advertisement

Advertisement

The contract was supported over the first half of the week but under pressure in the second half of the week. Oilseed markets fell with the broader commodity markets on technical selling and risk-off liquidation ahead of the long weekend in the US.

Further fuelling the pressure in oilseeds was the continued broader economic stress of recessional fears and pressure in crude oil markets. This seemed to overshadow the US acreage report released last Thursday which estimated soyabean plantings for harvest 22 at 88.33M acres, down 2.63M acres from March’s estimate, and 2.12M acres lower than trade estimates, read more information in Olivia’s Grain Market Daily.

In other oilseed news, Indonesia announced over the weekend that it was considering a larger export quota for palm oil to reduce high domestic inventories. Companies that have sold palm oil domestically will be able to export seven times their domestic sales (Refinitiv).

Also, Russia have also reduced their sunflower oil tax after altering the formula used to calculate it. This is to support shipments as the Rouble reaches multi-year highs (Refinitiv).

Advertisement

Advertisement

Over the coming week rains are forecast in much of the U.S. Midwest which could further add to price pressure as U.S. weather is current market focus.

Rapeseed focus

Paris rapeseed futures (Nov-22) trended lower last week and closed at €673/t on Friday, down by €18.75/t on the previous week. The May-23 contract closed at €669.75/t, down by €15/t. Rapeseed prices were under pressure in-line with global soya and palm oil markets.

Domestic delivered rapeseed price changes were unable to be published last week due to insufficient quotes to calculate the published average. The last quoted was published on 24 Jun (into Erith, Aug-22) at £566/t.

Canadian principal field crop areas will be released by StatCan. Based on a Refinitiv poll, the trade expects canola plantings to be revised upward to 21.3M acres in this report, up from the 20.9M acres estimated in April.